Writer: Indrabati Lahiri, Options Author

As local weather change and the inexperienced transition collect momentum in 2025, unlikely commodities comparable to copper and cocoa at the moment are reshaping world financial stability the way in which oil as soon as did. Copper costs have surged greater than 20 % up to now this yr, pushed by provide crunches, inexperienced infrastructure and knowledge centre demand. Equally, cocoa has seen excessive worth volatility, as a result of African local weather shocks, hitting report highs in early 2025, earlier than plummeting nearly 50 %.

Collectively, they spotlight a broader geopolitical shift away from fossil fuels in the direction of important commodities and pure sources. With copper driving the power transition and cocoa shaping meals provide chains and moral commerce, they’ve change into the twin bellwethers of a altering world order.

In addition they characterize how useful resource energy and strategic belongings are more and more concentrated within the International South, in West Africa’s cocoa heartlands and Latin America’s copper belt. In some ways, copper and cocoa at the moment are the ‘new oil’ – strategic, scarce and consultant of each innovation and world inequality.

Underpinning the local weather transition

Copper is crucial to electrification, being utilized in electrical automobiles, photo voltaic panels, wind generators, hydropower vegetation, grid upgrades and extra. Demand for copper from knowledge centres, the place it’s utilized in cooling methods, inside connectivity and energy methods, has elevated exponentially, supported by the surge in synthetic intelligence.

Based on the Worldwide Power Company (IEA), copper demand might hit 31.3 million tonnes by 2030, a substantial improve from 2021’s roughly 24.9 million tonnes. “China’s large grid enlargement and concrete improvement have been the only largest latest driver of copper demand. Continued Chinese language industrial stimulus and infrastructure spending are due to this fact key elements underpinning copper costs,” António Alvarenga, Professor of Technique and Entrepreneurship at Nova Faculty of Enterprise and Economics, defined. He added: “Nevertheless, copper mine output has grown solely about one to 2 % yearly, regardless of rising demand, and new tasks take round 15–17 years to develop.”

Copper manufacturing is very concentrated in Zambia and Democratic Republic of Congo, together with Latin America’s copper belt, together with Chile and Peru. “This focus of sources is quietly reshaping world alliances, as nations compete to safe long-term entry, very like the oil geopolitics of the twentieth century,” Sunil Kansal, head of Consulting and Valuation Providers at Shasat Consulting, stated.

Copper and cocoa mark a shift to the commodities of the longer term, scarce and economically resilient

As such, any mine accidents in these key nations can have a profound affect on copper manufacturing and drive costs up. Chile’s El Teniente mine had a lethal accident again in July this yr, which led to a serious manufacturing halt and drop in output. This was additionally seen on the Komoa-Kakula copper mine in DRC in April as a result of a flooding occasion and roof collapse. Older mines and continual underinvestment have boosted copper costs and precipitated provide chain bottlenecks too these days.

“Lots of the world’s main copper mines are growing old, and the common copper content material (ore grade) is declining, which means that extra rock have to be processed to extract the identical quantity of copper,” Franck Bekaert, senior rising markets analyst at Gimme Credit score, highlighted. “Moreover, allow delays and ecological constraints are hindering the launch of latest tasks, which is driving up prices. To fulfill the rising demand for copper, important investments will probably be required,” Bekaert added.

Political instability in main producing nations, comparable to employee strikes and environmental protests, in addition to governance points comparable to rising corruption have additionally contributed to produce woes. At current, copper inventories are at report lows, in accordance with Benchmark Intelligence, whilst inexperienced infrastructure demand from the US and EU soars.

Because the world races to impress, copper’s shortage is quick changing into a structural danger to world progress, very like oil shocks as soon as had been.

How local weather shocks affect cocoa

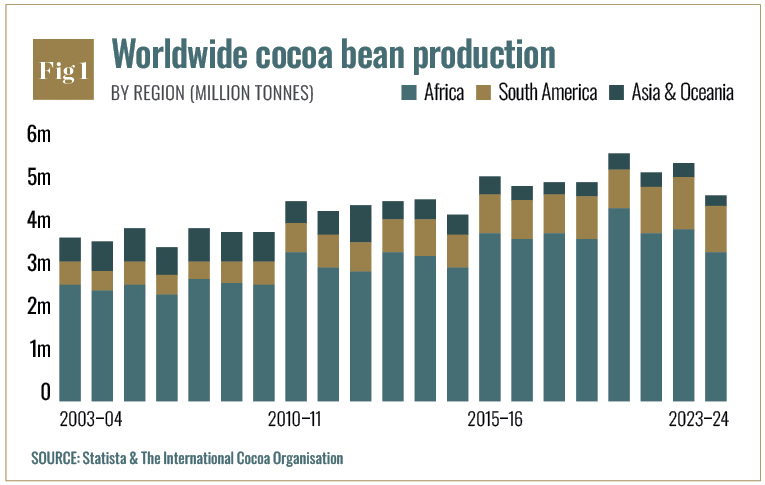

“When the Ivory Coast and Ghana sneeze, world chocolate catches a chilly. Cocoa simply had its ‘oil second’: a close to 500,000-ton world deficit in 2023–24 pushed inventories to multi-decade lows and despatched futures above $10,000/ton on the peak in January 2025,” Francisco Martin-Rayo, co-founder and CEO at Helios AI, stated. One of many largest causes for this was the El Niño climate sample within the 2023–24 season. This precipitated unstable climate patterns, comparable to unusually heavy rain, adopted by hotter and drier climate throughout key cocoa-producing nations comparable to Ghana and the Ivory Coast. Cocoa may be very delicate to climate modifications because it grows solely in restricted areas of heat, humid equatorial situations, with 70 % of the crop coming from West Africa (see Fig 1). These temperature extremes precipitated decreased cocoa yields and an increase in crop ailments comparable to swollen shoot virus and brown rot. The ailments additionally meant that the remaining yield was of decrease high quality, additional escalating costs. Getting old West African cocoa timber are one other issue contributing to larger costs. These can severely dampen yield capability due to decreased soil fertility. Older timber may also be extra susceptible to ailments and pests and change into weaker with time.

Farmers then want to speculate massive quantities in replanting and farm rehabilitation. Nevertheless, constantly low farmer incomes make such investments tough to take care of, making a vicious cycle of growing old timber, low productiveness and low incomes.

“Cocoa demand has grown steadily. Western vacation consumption and an increasing center class in Asia/Africa help baseline demand. Nevertheless, extraordinarily excessive costs can dampen consumption: in 2025 European and Asian cocoa grindings fell as producers confronted larger prices,” Alvarenga stated. The elements affecting cocoa transcend simply figuring out chocolate and associated product costs – they characterize a systemic disaster in agricultural provide chains right now, outlined by local weather volatility, worsening soil degradation and widespread farmer poverty. With a lot of the crop nonetheless tied to smallholder farmers, cocoa is a social commodity, intimately linked to human points comparable to meals insecurity, compelled migration and revenue loss and inequality, sitting on the coronary heart of debates about moral sourcing and truthful commerce. At the same time as costs pull again barely now, the structural points driving cocoa worth volatility stay.

Strategic belongings

Very similar to oil in previous a long time, each copper and cocoa provide has been extremely concentrated in just a few areas. This has considerably formed new geopolitical alignments and commerce tensions. One of many largest methods this has materialised is thru shoppers now actively looking for to diversify suppliers, to scale back provide chain and safety dangers. Copper, as a strategic steel and asset, is now essential to nations’ decarbonisation plans. As AI and different cutting-edge applied sciences collect tempo and require extra electrical energy, copper’s standing because the ‘new oil’ is prone to continue to grow. As such, main copper shoppers together with the US and EU at the moment are looking for extra suppliers to unfold provide dangers.

“The US launched a piece 232 nationwide safety investigation into copper and China has pivoted away from Chile by sourcing extra from DRC, Russia and Zambia. These strikes have created new alignments – comparable to China deepening ties with African producers, Western nations looking for different mines or stockpiles,” Alvarenga highlighted. This geopolitical strategising and positioning mimics previous useful resource wars over oil, creating new alliances between industrial powers and resource-rich nations. “As with oil, these relationships can result in commerce frictions, useful resource nationalism, and competitors for affect. For buyers, this focus magnifies geopolitical danger but additionally alerts long-term strategic worth,” Edward Nikulin, climate mannequin skilled at Thoughts Cash, stated.

For cocoa, Ghana and Ivory Coast’s governments wield appreciable provide affect via export laws and price-setting, appearing as a form of producer bloc, much like OPEC. “We’re seeing the emergence of coordinated motion by Ghana and the Ivory Coast to demand fairer phrases, echoing the useful resource diplomacy as soon as seen in oil markets,” Kansal stated. That is via the ‘Dwelling Earnings Differential,’ which raises export costs to make sure that extra cocoa revenue reaches farmers instantly to enhance residing requirements and scale back little one labour, poverty and deforestation.

“The joint $400/ton ‘Dwelling Earnings Differential’ set a de-facto flooring underneath farmgate economics, whereas EU deforestation guidelines (EUDR) are forcing farm-level traceability (GPS coordinates, plot IDs) and reshaping commerce flows towards compliant suppliers,” Martin-Rayo defined. “Count on extra native processing in Abidjan and San-Pédro and extra origin diversification to Ecuador/Brazil a traditional resource-security realignment.”

Cocoa farming is more and more utilizing extra tech comparable to satellite tv for pc imagery, robotic pollination, floor sensors and drones. These monitor pests, progress charges and soil moisture in massive plantations in actual time, serving to yields to change into extra secure, which may enhance cocoa’s financial and strategic significance. Equally, extra main copper corporations are specializing in accountable copper manufacturing practices, addressing sustainability and labour issues which are key to attracting the following technology of buyers. “Over the previous 5 years, copper and copper miners have considerably outpaced the S&P 500 and broad commodity indices. Devoted copper ETFs and mining shares have been well-liked. Upside for buyers comes from anticipated provide deficits: pent-up demand from EVs/renewables might raise costs if new mine output lags,” Alvarenga stated.

Nevertheless, he emphasised that coverage intervention dangers like stockpiling and tariffs stay, which might out of the blue lower copper flows. Though cocoa is extra unstable and speculative than copper, Martin-Rayo calls its oil-like standing a regime shift. “Consider cocoa as smaller than oil, however newly ‘systemic’ for meals producers and retailers.”

The highway forward

2025 highlights the beginning of a ‘post-oil’ useful resource period – one the place sustainable and moral commodities maintain energy. The ‘new oil’ could also be mined, grown or digitally verifiable, as an alternative of liquid. Each copper and cocoa mark a shift to the commodities of the longer term, scarce and economically resilient in an more and more fragmented world, with buyers demanding stability between transparency, accountability and progress.

Source link

#Copper #cocoa #geography #energy