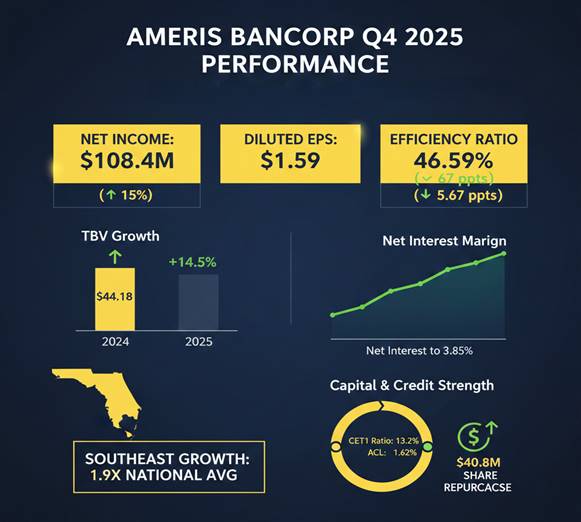

Ameris Bancorp (Nasdaq: ABCB) reported a considerable enhance in fourth-quarter earnings for 2025, supported by increasing curiosity margins and considerably improved operational effectivity. The Atlanta-based regional lender posted web earnings of $108.4 million, or $1.59 per diluted share, representing a 15% enhance in contrast with the $94.4 million reported in the identical interval of 2024.

Core Monetary Efficiency

The financial institution’s fourth-quarter outcomes have been highlighted by a tax-equivalent web curiosity margin (NIM) growth to three.85%, up 5 foundation factors from the third quarter and 21 foundation factors from the prior yr. This margin growth fueled web curiosity earnings (TE) of $246.3 million, a ten.6% enhance over the fourth quarter of 2024.

For the total fiscal yr 2025, Ameris recorded web earnings of $412.2 million, or $6.00 per diluted share, up from $358.7 million in 2024.

Key profitability metrics for the yr included:

Return on Common Property (ROA): 1.54% (up from 1.38% in 2024)

Return on Common Tangible Widespread Fairness (ROTCE): 14.51%

Tangible E book Worth (TBV) Development: Elevated 14.5% year-over-year to $44.18 per share

Operational self-discipline remained a central theme, because the financial institution’s effectivity ratio improved to 46.59% within the fourth quarter, down from 52.26% a yr in the past. Whole noninterest bills for the quarter have been $143.1 million, a lower of roughly $11.5 million from the third quarter. This discount was pushed primarily by decrease incentive compensation and healthcare prices inside the core banking division, alongside lowered mortgage servicing bills following mortgage servicing proper (MSR) gross sales.

Mortgage Portfolio and Asset High quality

Ameris reported incomes asset progress of $374.0 million within the ultimate quarter, an annualized enhance of 5.9%. Whole loans grew by $255.1 million throughout the interval, regardless of greater than $500 million in payoffs inside the investor business actual property (CRE) and multi-family segments. Mortgage manufacturing reached $2.4 billion for the quarter, the best degree recorded since 2022 and a 37% enhance over the fourth quarter of 2024.

The financial institution’s mortgage portfolio stays diversified, with investor CRE and business and industrial (C&I) loans every representing roughly 25-26% of the $21.5 billion whole stability.

Credit score high quality metrics have been characterised by administration as steady:

Allowance for Credit score Losses (ACL): Maintained at 1.62% of whole loans.

Web Cost-Offs (NCOs): Totaled 0.18% of common whole loans for the total yr.

Non-Performing Property (NPAs): Stood at 0.44% of whole property, with 35.5% of those property consisting of government-guaranteed mortgages.

Deposits and Capital Administration

The deposit base grew to $22.4 billion at year-end, a 3.0% enhance for the total yr. Noninterest-bearing deposits remained a power, accounting for 28.7% of the overall deposit combine. The financial institution famous seasonal public fund inflows of $892.6 million within the fourth quarter, which offset a lower of $744.3 million in non-brokered, personal fund deposits.

Administration continues to emphasise capital power, reporting a Widespread Fairness Tier 1 (CET1) ratio of 13.2% and a Tangible Widespread Fairness (TCE) ratio of 11.4%. In the course of the fourth quarter, the financial institution repurchased 563,798 shares of widespread inventory for $40.8 million. As of December 31, 2025, roughly $159.2 million stays accessible beneath the present $200 million share repurchase authorization.

Technique and Market Outlook

Ameris management maintains a deal with high-growth Southeast markets—together with Atlanta, Jacksonville, and Savannah—the place inhabitants progress is projected to outpace the nationwide common by roughly 1.9 occasions over the following 5 years.

Relating to future rate of interest environments, the financial institution’s inner modeling suggests it’s close to rate of interest neutrality. Administration famous that roughly $12.5 billion in whole loans are scheduled to reprice inside one yr by way of maturities or floating price indices, positioning the establishment for potential shifts in federal financial coverage.

Causes to Move on ABCB

- Web curiosity margin close to peak, with administration indicating the stability sheet is near rate of interest neutrality.

- Earnings progress pushed primarily by funding value reductions, not larger asset yields.

- Sequential decline in noninterest earnings, reflecting weaker mortgage banking exercise.

- Excessive mortgage payoffs offset manufacturing, requiring elevated origination volumes to maintain modest web mortgage progress.

- Significant publicity to investor CRE and multifamily loans, collectively accounting for roughly half of whole loans.

- Deposit progress supported by seasonal public funds, whereas non-brokered, personal deposits declined.

- Expense enhancements partly tied to variable objects, similar to incentive compensation and healthcare prices.

- Restricted near-term upside to credit score prices, with reserves maintained and provisioning ongoing.

- Average progress outlook, with no indication of accelerating stability sheet or earnings growth.

Commercial

Source link

#Ameris #Bancorp #Reviews #Earnings #Development #Improves #Working #Effectivity #AlphaStreet