Image source: Getty Images

A cheap share doesn’t necessarily mean it’s worth buying. Investors may have good reasons to be nervous about a company’s prospects. Indeed, following on from mechanisation, electrification and automation, we’re now in an era of digitialisation with artificial intelligence (AI) leading the way.

Inevitably, there will be winners and losers from the fourth industrial revolution. And judging by the share price performance of these three stocks, investors have already made up their minds about who the losers might be. But could this be a potential buying opportunity?

Hazel’s here!

The St James’s Place (LSE:STJ) share price has come under pressure after Altruist, an online provider of services to investment advisors, launched Hazel, its new AI tax planning tool.

For up to $150 a month (large firms will pay more), the US company claims its new software will “transform your practice” with interactive scenario modelling. Although the tool itself is unlikely to directly impact St James’s Place, it raises questions as to what might follow.

In 2024, the wealth manager charged £1.089bn for investment advice, 34% of its total income. And even if its clients would rather rely on humans for advice, AI could open up the market to low-cost challengers.

The timing of the arrival of Hazel’s unfortunate. Over the course of 2025, the group’s assets under management increased by £29.8bn, helped by net inflows of £6.2bn and a 94.9% retention rate.

However, even though the stock’s trading close to its 52-week low, I don’t want to invest given the uncertainty.

What about Claude?

By contrast, I like the look of London Stock Exchange Group (LSE:LSEG). I think it remains a stock to consider even though its share price is coming under pressure from anxiety about how Anthropic’s AI-powered legal assistant, an add-on to its Claude platform, could impact data and software companies.

Again, the software itself isn’t a particular threat, but what’s coming down the line? However, I think AI could work to LSEG’s advantage. The technology requires data, which the group has in bucket loads. Its propriety data’s spread across five distinct operating divisions.

Elliott Management appears to agree with me. The Financial Times claims the activist investor has been building up a “significant” stake. The firm’s established a reputation for investing in underperforming companies.

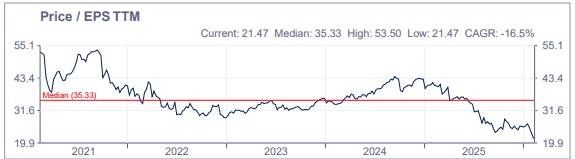

LSEG’s shares are now trading at their lowest earnings multiple since the pandemic. And they’re changing hands for what they were in the first quarter of 2023. I think the stock offers good value and is worth considering.

And finally…

Another stock under the AI cosh is MONY Group (LSE:MONY), owner of a number of websites designed to save households cash, including MoneySupermarket. Its share price is now back to where it was in 2013.

It’s been affected by Insurify, another US company, releasing what it claims is the insurance industry’s first ChatGPT app. Drivers will be able to explore personalised quotes.

MONY Group’s vulnerable because, in 2024, it generated nearly 54% of its revenue from insurance referrals. Obtaining quotes though ChatGPT sounds appealing to me, especially if it avoids having to answer all those tedious questions that are usually asked.

The direction of travel is clear and I’m not sure what the group can do about it. For this reason, investing now would be too risky for me.

Source link

#disruption #cheap #shares #bargain #buys