Shares Slide as Income Miss Offsets Raised Working Steerage | AlphaStreet – Imperial Wire")

By Workers Correspondent |

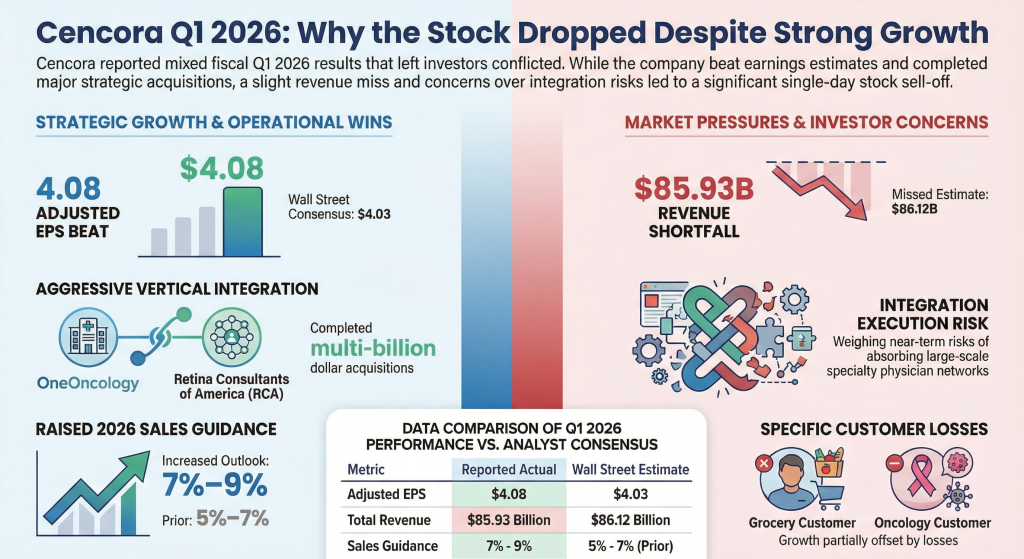

Shares of Cencora, Inc. (NYSE: COR) fell 8.8% to shut at $329.85 on Wednesday, as traders weighed a marginal income miss and a pointy decline in worldwide working revenue towards an improved full-year working outlook. The inventory gapped down on the open regardless of an adjusted earnings beat, marking its steepest one-day decline in over a 12 months.

Firm Description

Cencora, Inc. is a world pharmaceutical options firm that sources and distributes brand-name, generic, and specialty prescription drugs. The corporate supplies providers to healthcare suppliers and pharmaceutical producers, together with medical trial logistics, market entry consulting, and specialty doctor providers. It operates via two foremost segments: U.S. Healthcare Options and Worldwide Healthcare Options, following its strategic pivot towards high-margin specialty healthcare platforms.

Market Efficiency and Valuation

- Present Inventory Worth: $329.85 (Shut Feb 4, 2026)

- Market Capitalization: Roughly $64.05 billion

- 52-Week Context: The inventory has traded between $237.71 and $377.54 over the previous 12 months. Wednesday’s decline worn out roughly $6 billion in market worth.

- Valuation: Cencora trades at a ahead P/E of 18.7x primarily based on the $17.60 midpoint of its fiscal 2026 steerage. This a number of stays above its historic five-year common, reflecting the market’s premium on its increasing oncology and specialty medication footprint.

Fiscal First Quarter 2026 Outcomes

Cencora reported monetary outcomes for the quarter ended December 31, 2025:

- Income: $85.93 billion, up 5.5% year-over-year, lacking the $86.03 billion consensus estimate.

- Adjusted Diluted EPS: $4.08, up 9.4% from $3.73 within the prior-year interval, beating the $4.04 analyst consensus.

- Adjusted Gross Margin: Expanded 37 foundation factors to three.48%, primarily pushed by the Retina Consultants of America (RCA) acquisition.

- Phase Efficiency:

- U.S. Healthcare Options: Income rose 5% to $76.2 billion; working revenue surged 21% to $831.3 million, fueled by sturdy demand for GLP-1 (weight reduction) and oncology therapies.

- Worldwide Healthcare Options: Income elevated 9.6% to $7.6 billion, however working revenue fell 13.9% (down 17% on a continuing foreign money foundation) because of unfavorable producer worth changes in a growing market.

Up to date 2026 Steerage and Forecasts

The corporate up to date its full-year outlook to replicate the completion of the OneOncology acquisition:

- Working Earnings: Progress steerage raised to 11.5%–13.5% (from 8%–10%).

- Income Progress: Raised to 7%–9% (from 5%–7%).

- Adjusted EPS: Reaffirmed at $17.45 to $17.75, with the midpoint of $17.60 falling barely beneath the analyst consensus of $17.62.

- Curiosity Expense: Full-year expectation elevated to $480 million–$500 million because of financing prices for latest M&A.

Macro Pressures and Threat Components

- Geopolitical/Worldwide: Profitability within the Worldwide section was hampered by the timing of regulatory worth resets in Europe and growing markets. Administration expects this to unwind however stays cautious on foreign money volatility.

- Tariff & Commerce: Whereas not a direct importer of completed items impacted by present electronics tariffs, the corporate famous that international logistics prices for its World Courier enterprise stay delicate to commerce coverage shifts.

- Leverage: The corporate reported damaging adjusted free money circulation of $2.4 billion within the quarter (seasonal) and has paused share repurchases to prioritize debt paydown after the OneOncology closing.

SWOT Evaluation

| Strengths | Weaknesses |

| Management in specialty/oncology distribution (OneOncology integration). | Income miss highlights sensitivity to high-volume pharmacy quantity shifts. |

| Sturdy U.S. working revenue progress (+21% in Q1). | Excessive curiosity expense ($480M+) weighing on web revenue progress. |

| Alternatives | Threats |

| Continued excessive demand for GLP-1 and immunology therapies. | Regulatory scrutiny of PBM/Wholesaler pricing and “clawbacks.” |

| Enlargement of high-margin commercialization providers for biopharma. | Worldwide working revenue volatility and foreign money headwinds. |

Commercial

Source link

#Cencora #COR #Shares #Slide #Income #Offsets #Raised #Working #Steerage #AlphaStreet